Corpay’s Use of JPMorgan’s Kinexys Blockchain Could Be a Game Changer for JPM (JPM)

- Earlier this month, Corpay Inc. announced that its Cross-Border business can now facilitate client FX conversions using J.P. Morgan's Kinexys Digital Payments blockchain, enabling near real-time value transfer and settlement beyond traditional banking hours.

- This marks a meaningful advancement in the use of blockchain for cross-border payments, expanding operational flexibility and demonstrating the practical impact of JPMorgan Chase's technology investments.

- With this partnership highlighting blockchain's growing role in global payments, we'll explore how it shapes JPMorgan Chase's investment narrative moving forward.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

JPMorgan Chase Investment Narrative Recap

To be a JPMorgan Chase shareholder today, you need conviction in the firm’s ability to maintain leadership through technology, scale, and a diversified financial platform. The Corpay-Kinexys blockchain partnership is a positive sign for payment innovation, but by itself is unlikely to materially shift the most important short-term catalyst: continued growth in digital payments and fee-based revenue. The biggest risk remains mounting digital disruption and aggressive fintech competition, factors not fundamentally altered by the announcement.

Among the recent announcements, JPMorgan Chase’s increased technology budget to US$18 billion in 2025 stands out as closely relevant. This substantial investment supports advances like Kinexys and signals ongoing commitment to digital transformation, a vital catalyst for strengthening competitive positioning against fintechs and supporting new revenue streams. These actions may not resolve all risks, but they reinforce the firm’s strategic direction toward innovation-driven growth.

Still, on the other hand, investors should keep in mind that intensifying digital competition and evolving fintech risks are far from the only threats they might face...

Read the full narrative on JPMorgan Chase (it's free!)

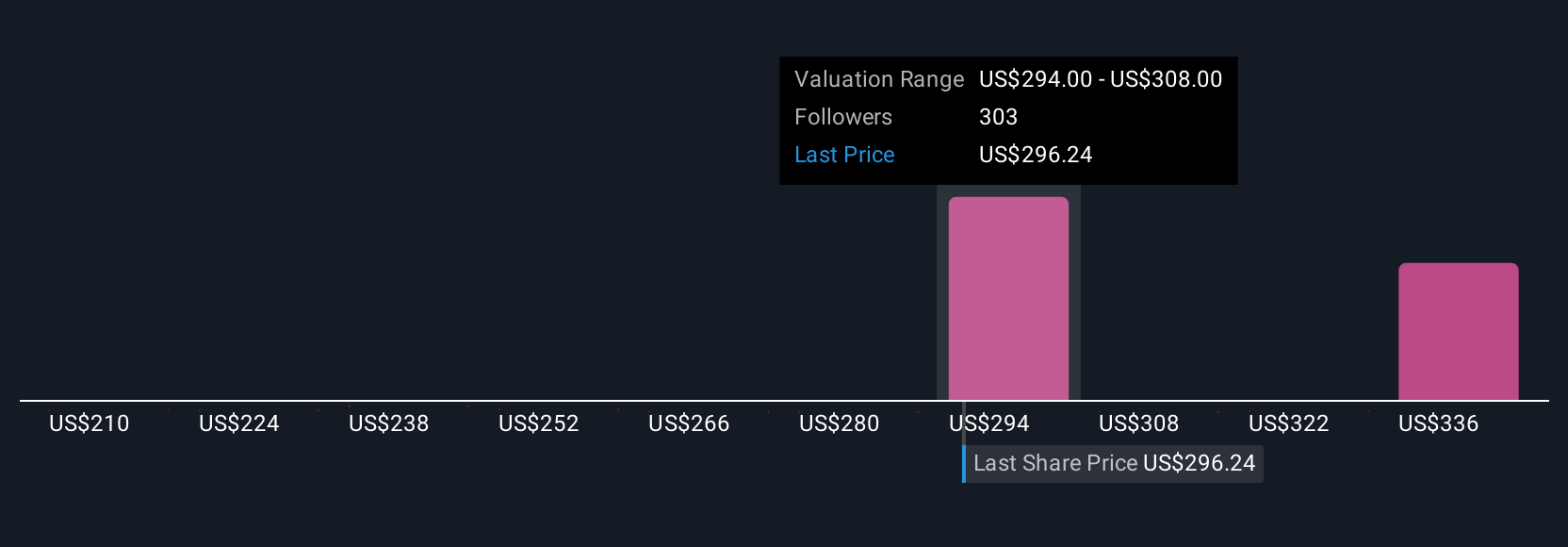

JPMorgan Chase is projected to generate $187.9 billion in revenue and $55.6 billion in earnings by 2028. This outlook is based on an expected annual revenue growth rate of 4.7% and assumes earnings will increase by about $0.4 billion from current earnings of $55.2 billion.

Uncover how JPMorgan Chase's forecasts yield a $305.81 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Lowest analyst estimates warned of higher expenses and credit losses, forecasting 2028 earnings of only US$53.2 billion. Their view is much more pessimistic than consensus and highlights the need to consider alternative scenarios as major news events emerge that could shift analyst sentiment over time.

Explore 25 other fair value estimates on JPMorgan Chase - why the stock might be worth as much as 19% more than the current price!

Build Your Own JPMorgan Chase Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your JPMorgan Chase research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free JPMorgan Chase research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate JPMorgan Chase's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10