Did Autohome’s (ATHM) Earnings Miss and Share Buyback Reveal a Shift in Its Capital Strategy?

- Autohome announced its second quarter 2025 results, reporting revenue of CNY 1,758.12 million and net income of CNY 398.87 million, both lower than the prior year, while also completing a buyback of 5,349,886 shares for US$142.4 million as of July 25, 2025.

- Despite an earnings miss and slower anticipated growth, Autohome's continued buybacks could support shareholder confidence amid ongoing operational challenges.

- Next, we'll examine how Autohome’s recently completed share buyback may influence its long-term investment outlook and earnings potential.

Find companies with promising cash flow potential yet trading below their fair value.

Autohome Investment Narrative Recap

To own shares of Autohome, an investor needs to believe in the company’s ability to leverage Haier Group’s partnership, strengthen its brand, and expand into new growth areas, even as market competition intensifies. The recent earnings miss and declining year-over-year revenue and net income highlight softening demand and profitability pressure, but do not materially shift the key near-term catalyst, the anticipated effects of Haier’s integration, nor the major risk, which remains execution uncertainty around that transition.

Autohome’s completion of its share buyback program, repurchasing 5,349,886 shares for US$142.4 million, stands out. This move is particularly relevant as it may support earnings per share and signals ongoing management confidence, even as the company faces challenges from slower revenue growth and margin compression. Despite these efforts, investors should be aware that the biggest risk right now could come from integration setbacks...

Read the full narrative on Autohome (it's free!)

Autohome's narrative projects CN¥7.4 billion in revenue and CN¥1.8 billion in earnings by 2028. This requires 2.2% yearly revenue growth and a CN¥0.2 billion earnings increase from CN¥1.6 billion today.

Uncover how Autohome's forecasts yield a $29.15 fair value, a 6% upside to its current price.

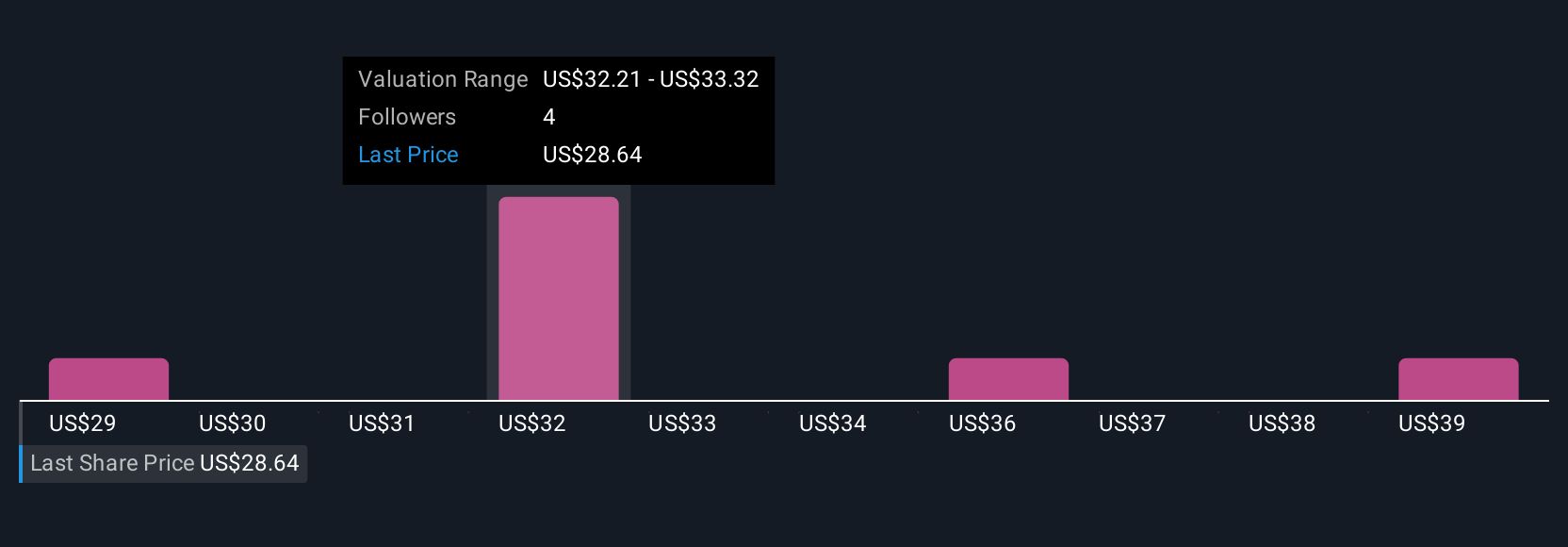

Exploring Other Perspectives

Simply Wall St Community members published 4 fair value estimates for Autohome ranging from US$29.15 to US$40. With this wide span of investor opinions, keep in mind that ongoing execution risks tied to Haier integration may have broad implications for future results.

Explore 4 other fair value estimates on Autohome - why the stock might be worth as much as 45% more than the current price!

Build Your Own Autohome Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Autohome research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Autohome research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Autohome's overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 25 companies in the world exploring or producing it. Find the list for free.

- These 19 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10