Earnings Misses and Rising Revenues Might Change the Case for Investing in Evergy (EVRG)

- Wall Street analysts expect Evergy to report a year-over-year decline in earnings for the quarter ended June 2025, even as revenues are projected to rise, with the company's next earnings report scheduled for August 7.

- Market sentiment has been shaped by Evergy’s recent history of frequently missing earnings estimates, prompting investors to closely watch how actual results compare to expectations.

- With investor attention fixed on Evergy’s upcoming earnings report and its track record of earnings misses, we’ll explore how this shapes the company’s investment outlook.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Evergy Investment Narrative Recap

To be a shareholder in Evergy is to have confidence in the company’s ability to execute its ambitious $17.5 billion capital investment plan, modernize its grid, and deliver steady returns despite regulatory and weather-related risks. The recent news of anticipated earnings decline, even with rising revenues, places heightened significance on upcoming quarterly results, but does not materially alter the central short-term catalyst: successful infrastructure execution. The primary risk remains cost overruns or funding issues tied to these major investments.

Among the latest announcements, Evergy’s $1.2 billion follow-on equity offering is most relevant, as it directly impacts capital structure and the funding for its large-scale infrastructure projects. This move connects closely to the core catalyst of grid investment and the related risk of shareholder dilution if capital requirements outpace earnings growth.

However, it’s important to also recognize that while infrastructure investment may lead to growth, investors should pay attention to...

Read the full narrative on Evergy (it's free!)

Evergy's narrative projects $6.7 billion revenue and $1.1 billion earnings by 2028. This requires 4.5% yearly revenue growth and a $224.2 million earnings increase from $875.8 million.

Uncover how Evergy's forecasts yield a $74.45 fair value, a 4% upside to its current price.

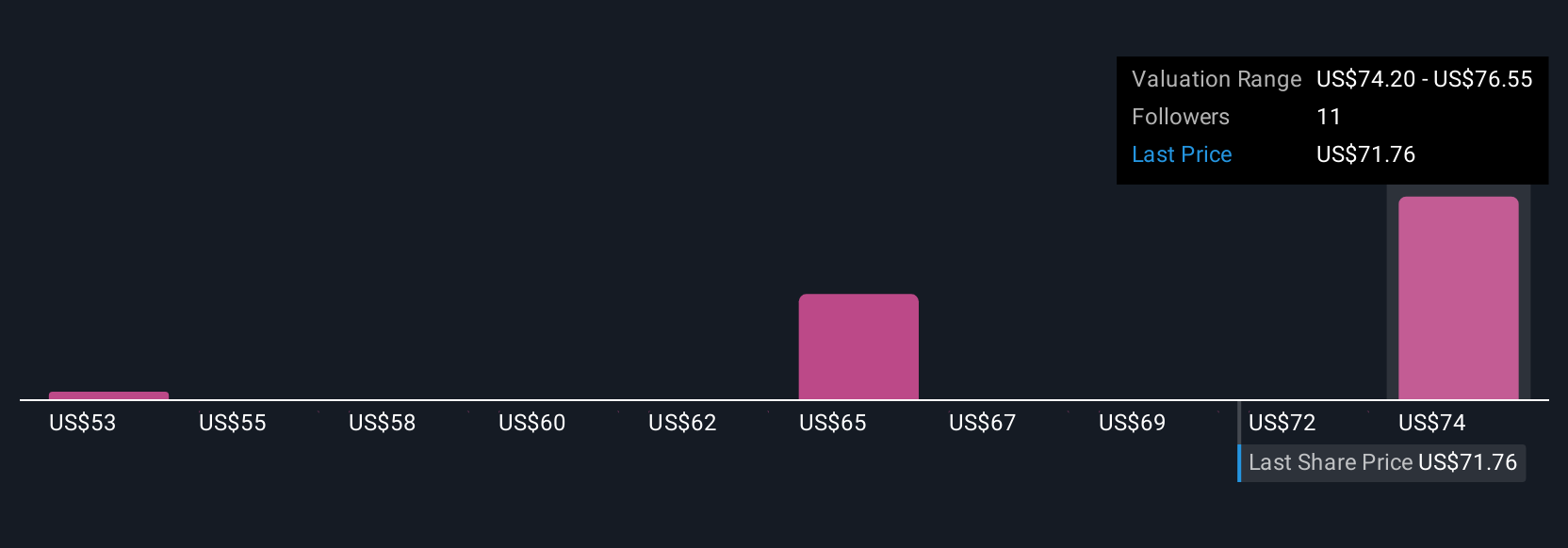

Exploring Other Perspectives

Three individual fair value estimates from the Simply Wall St Community span US$53 to US$74.45 per share. With diverse views, especially around Evergy’s ability to manage financial risks in its investment plan, you can compare several opinions here for a broader understanding of future performance drivers.

Explore 3 other fair value estimates on Evergy - why the stock might be worth as much as $74.45!

Build Your Own Evergy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Evergy research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Evergy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Evergy's overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- We've found 22 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Evergy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10