TradingKey - On President Donald Trump’s argument that firing Fed Chair Jerome Powell would lower interest rates and reduce the U.S. government’s soaring debt costs, Deutsche Bank has issued a clear warning: forced rate cuts would have little meaningful impact on debt burdens, and could even increase long-term borrowing costs.

In a report published on July 23, Deutsche Bank economists stated that removing Powell would not reduce the U.S. Treasury’s interest expenses — despite Trump’s repeated claims that aggressive rate cuts could save hundreds of billions in debt servicing.

Since Trump’s return to the White House, his campaign to pressure Powell into cutting rates has become a global financial market drama. To finance massive tax cuts and manage record-high U.S. debt, Trump has openly demanded that the Fed cut interest rates immediately.

Beyond inflation control, Trump has cited lowering Treasury interest costs, concerns over Fed headquarters renovation spending, and supporting the housing market as reasons for rate cuts. He has even argued that U.S. rates should fall by 3 percentage points — or more.

Trump has claimed that:

- A 300-basis-point cut could save the U.S. government over $1 trillion

- A 200-basis-point cut would save $600 billion per year in interest costs

Deutsche Bank’s Reality Check

Deutsche Bank disagrees sharply.

Even if firing Powell leads to 50 additional basis points of easing beyond current expectations, the Treasury would only save $12–15 billion per year through 2027 — a negligible amount relative to total debt.

The bank’s analysis of the July 16 “one-hour firing scare” revealed a critical dynamic:

- Short-term yields fell due to expectations of more dovish policy

- But long-term yields rose on fears of higher inflation and Fed politicization

This means that any savings from lower short-term rates could be offset — or even exceeded — by higher long-term borrowing costs.

The Risk of Backfiring

Deutsche Bank is not alone in this view.

- JPMorgan warned that unless supported by strong economic fundamentals, rate cuts could reignite inflation, leading to higher nominal rates over time

- Nomura noted that while short-term rate cuts may temporarily reduce interest costs, the resulting rise in inflation expectations could quickly erase those savings

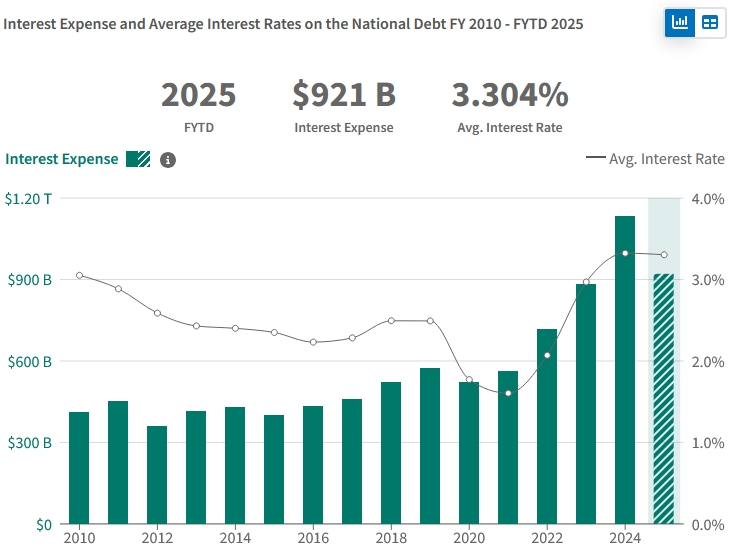

Since the Fed began its aggressive hiking cycle in 2022 to combat post-pandemic inflation, U.S. debt servicing costs have surged. In the first nine months of FY2025, interest payments reached $921 billion, up 6% YoY.

U.S. Treasury Interest Costs, Source: FiscalData

What If Rates Fall Sharply?

Deutsche Bank acknowledged that if Trump succeeds in forcing rates down to 1%, the savings could be larger. But such a scenario would likely trigger even more extreme market reactions — with long-term yields spiking due to inflation fears — potentially increasing overall debt costs.

Even in a best-case scenario where long-term rates fall due to expectations of a prolonged low-rate environment, the net savings may still be limited.

If the entire yield curve drops by 50 basis points, Deutsche Bank estimates the Treasury could save $78 billion through 2027 — still a small fraction of total debt.

The bank concluded that the actual impact depends on highly uncertain factors, including:

- How long the Fed maintains an accommodative stance

- How much investors demand in inflation compensation

- Whether Fed independence is perceived as compromised

Find out more