Asian Stocks Estimated To Be Trading At Discounts Of Up To 26.6%

As global markets navigate the complexities of new tariffs and shifting economic policies, Asian stock indices have shown resilience, with some regions even experiencing modest gains. In this context, identifying undervalued stocks in Asia can be particularly appealing for investors looking to capitalize on potential discounts. A good stock in such an environment is one that demonstrates strong fundamentals and the ability to withstand market fluctuations while trading below its intrinsic value.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Wenzhou Yihua Connector (SZSE:002897) | CN¥38.39 | CN¥75.06 | 48.9% |

| Range Intelligent Computing Technology Group (SZSE:300442) | CN¥52.97 | CN¥104.19 | 49.2% |

| Ningbo Sanxing Medical ElectricLtd (SHSE:601567) | CN¥23.06 | CN¥46.09 | 50% |

| Nanya Technology (TWSE:2408) | NT$41.75 | NT$82.05 | 49.1% |

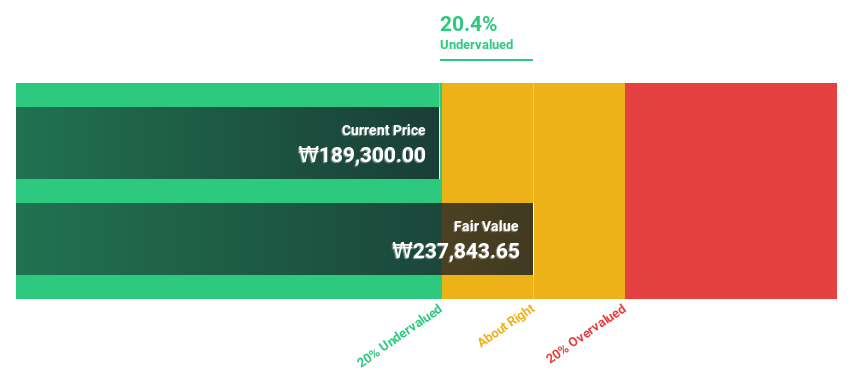

| Medy-Tox (KOSDAQ:A086900) | ₩161300.00 | ₩322233.66 | 49.9% |

| Maxscend Microelectronics (SZSE:300782) | CN¥70.97 | CN¥138.00 | 48.6% |

| Hugel (KOSDAQ:A145020) | ₩357500.00 | ₩698441.84 | 48.8% |

| HL Holdings (KOSE:A060980) | ₩42300.00 | ₩82760.82 | 48.9% |

| cottaLTD (TSE:3359) | ¥428.00 | ¥854.19 | 49.9% |

| ALUX (KOSDAQ:A475580) | ₩11460.00 | ₩22618.64 | 49.3% |

Click here to see the full list of 266 stocks from our Undervalued Asian Stocks Based On Cash Flows screener.

Let's dive into some prime choices out of the screener.

Celltrion (KOSE:A068270)

Overview: Celltrion, Inc. is a biopharmaceutical company focused on developing, producing, and selling therapeutic proteins for oncology treatments with a market capitalization of approximately ₩39.45 trillion.

Operations: The company's revenue primarily comes from biopharmaceuticals, contributing ₩6.18 trillion, followed by chemical drugs at ₩523.71 billion.

Estimated Discount To Fair Value: 10.7%

Celltrion's stock appears undervalued based on cash flows, trading at ₩178,600, below its estimated fair value of ₩200,109.89. The company's recent share repurchase program aims to stabilize the stock price and enhance shareholder value. Celltrion's earnings are forecasted to grow significantly at 27.1% annually over the next three years, outpacing the Korean market average of 20.7%. Recent FDA approvals for biosimilars bolster its product portfolio and potential revenue streams.

- Our earnings growth report unveils the potential for significant increases in Celltrion's future results.

- Click here and access our complete balance sheet health report to understand the dynamics of Celltrion.

Akeso (SEHK:9926)

Overview: Akeso, Inc. is a biopharmaceutical company involved in the research, development, manufacture, and commercialization of antibody drugs globally with a market cap of HK$108.34 billion.

Operations: The company generates revenue of CN¥2.12 billion from its activities in the research, development, production, and sale of biopharmaceutical products.

Estimated Discount To Fair Value: 20.6%

Akeso's stock, trading at HK$120.7, is undervalued relative to its estimated fair value of HK$151.97, presenting a potential opportunity based on cash flows. The company's robust pipeline includes innovative bispecific antibodies like cadonilimab and ivonescimab, which have achieved significant regulatory approvals across multiple regions. With revenue forecasted to grow at 29.8% annually and the company expected to become profitable within three years, Akeso's strategic advancements in immunotherapy could enhance its financial performance significantly.

- Our expertly prepared growth report on Akeso implies its future financial outlook may be stronger than recent results.

- Unlock comprehensive insights into our analysis of Akeso stock in this financial health report.

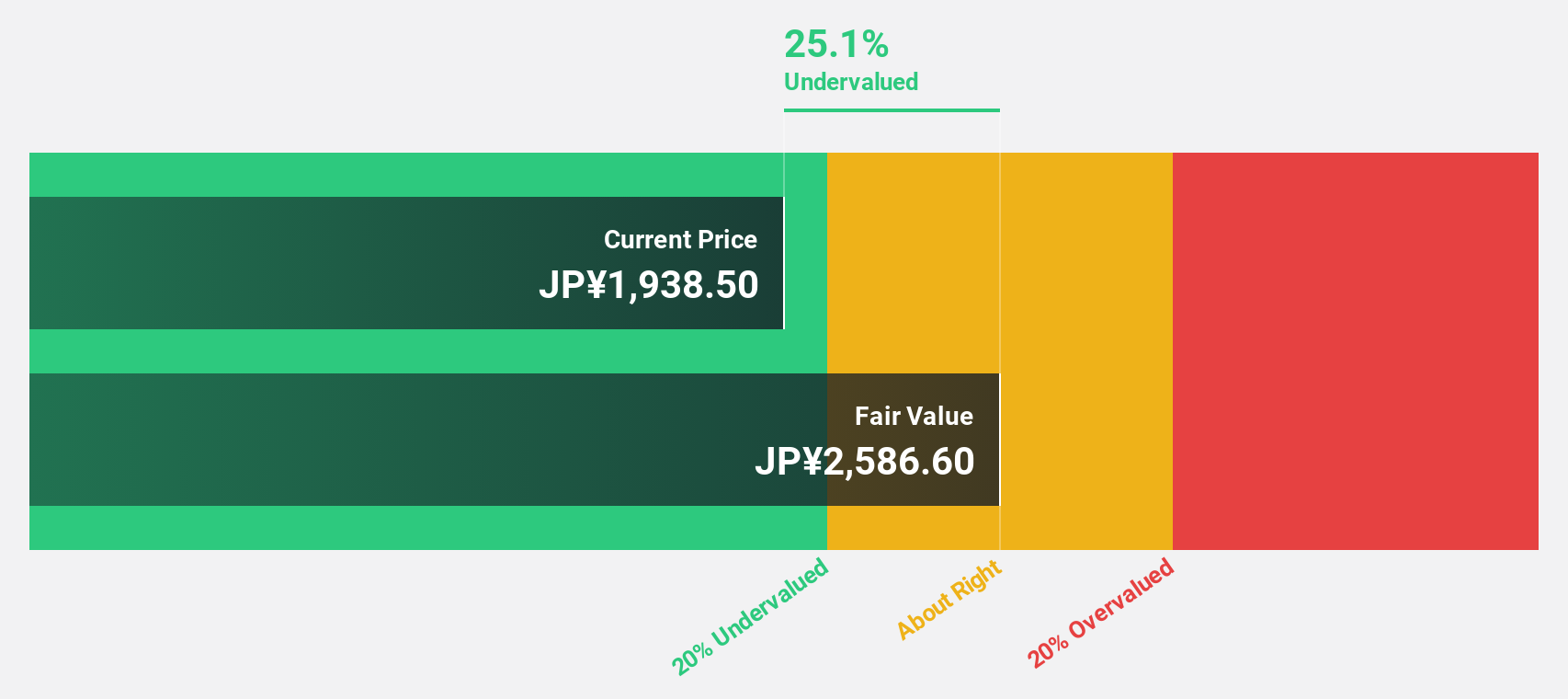

Sawai Group Holdings (TSE:4887)

Overview: Sawai Group Holdings Co., Ltd. operates in the research and development, manufacturing, and marketing of generic pharmaceuticals, with a market capitalization of ¥219.30 billion.

Operations: Sawai Group Holdings Co., Ltd. generates revenue primarily through its activities in the research and development, production, and distribution of generic pharmaceuticals.

Estimated Discount To Fair Value: 26.6%

Sawai Group Holdings is trading at ¥1,899.5, significantly below its estimated fair value of ¥2,586.6, suggesting it may be undervalued based on cash flows. Despite a decline in profit margins from 9.7% to 1.1%, the company's earnings are forecasted to grow at 24.2% annually, outpacing the Japanese market's average growth rate of 7.7%. However, the dividend yield of 2.9% lacks adequate coverage by earnings or free cash flows, posing potential sustainability concerns.

- The growth report we've compiled suggests that Sawai Group Holdings' future prospects could be on the up.

- Click here to discover the nuances of Sawai Group Holdings with our detailed financial health report.

Turning Ideas Into Actions

- Dive into all 266 of the Undervalued Asian Stocks Based On Cash Flows we have identified here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10