Williams-Sonoma Insiders Sold US$2.8m Of Shares Suggesting Hesitancy

In the last year, many Williams-Sonoma, Inc. (NYSE:WSM) insiders sold a substantial stake in the company which may have sparked shareholders' attention. When analyzing insider transactions, it is usually more valuable to know whether insiders are buying versus knowing if they are selling, as the latter sends an ambiguous message. However, if numerous insiders are selling, shareholders should investigate more.

While insider transactions are not the most important thing when it comes to long-term investing, we would consider it foolish to ignore insider transactions altogether.

We've found 21 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

The Last 12 Months Of Insider Transactions At Williams-Sonoma

In the last twelve months, the biggest single sale by an insider was when the insider, Karalyn Smith, sold US$1.5m worth of shares at a price of US$135 per share. So it's clear an insider wanted to take some cash off the table, even below the current price of US$173. We generally consider it a negative if insiders have been selling, especially if they did so below the current price, because it implies that they considered a lower price to be reasonable. Please do note, however, that sellers may have a variety of reasons for selling, so we don't know for sure what they think of the stock price. We note that the biggest single sale was only 42% of Karalyn Smith's holding.

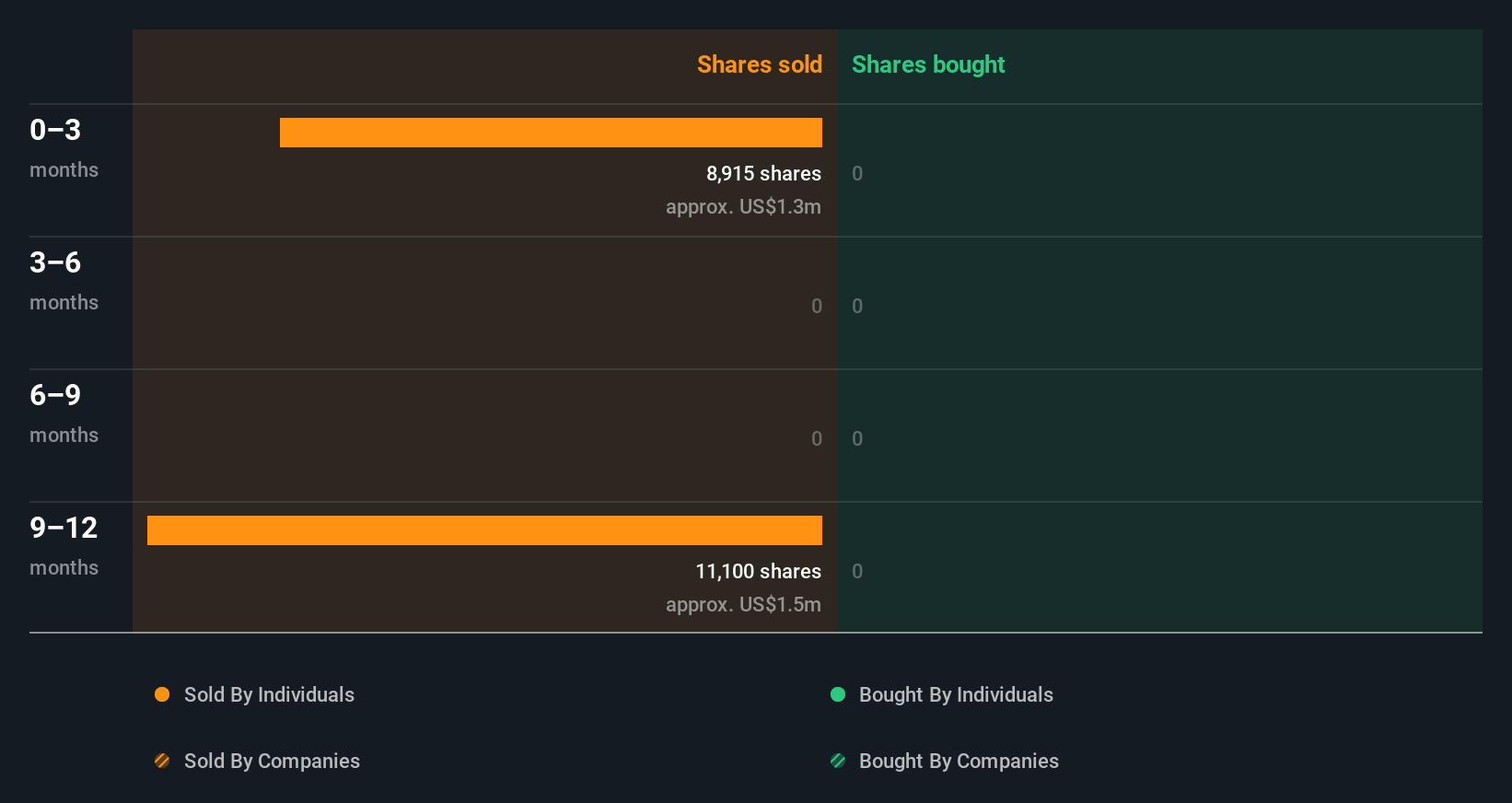

In the last year Williams-Sonoma insiders didn't buy any company stock. The chart below shows insider transactions (by companies and individuals) over the last year. If you want to know exactly who sold, for how much, and when, simply click on the graph below!

See our latest analysis for Williams-Sonoma

If you are like me, then you will not want to miss this free list of small cap stocks that are not only being bought by insiders but also have attractive valuations.

Williams-Sonoma Insiders Are Selling The Stock

The last three months saw significant insider selling at Williams-Sonoma. In total, insiders dumped US$1.3m worth of shares in that time, and we didn't record any purchases whatsoever. This may suggest that some insiders think that the shares are not cheap.

Insider Ownership

I like to look at how many shares insiders own in a company, to help inform my view of how aligned they are with insiders. Usually, the higher the insider ownership, the more likely it is that insiders will be incentivised to build the company for the long term. Williams-Sonoma insiders own about US$236m worth of shares (which is 1.1% of the company). I like to see this level of insider ownership, because it increases the chances that management are thinking about the best interests of shareholders.

What Might The Insider Transactions At Williams-Sonoma Tell Us?

Insiders sold Williams-Sonoma shares recently, but they didn't buy any. And there weren't any purchases to give us comfort, over the last year. But it is good to see that Williams-Sonoma is growing earnings. While insiders do own a lot of shares in the company (which is good), our analysis of their transactions doesn't make us feel confident about the company. While it's good to be aware of what's going on with the insider's ownership and transactions, we make sure to also consider what risks are facing a stock before making any investment decision. While conducting our analysis, we found that Williams-Sonoma has 1 warning sign and it would be unwise to ignore it.

But note: Williams-Sonoma may not be the best stock to buy. So take a peek at this free list of interesting companies with high ROE and low debt.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions of direct interests only, but not derivative transactions or indirect interests.

Valuation is complex, but we're here to simplify it.

Discover if Williams-Sonoma might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10