- ASTS holds $874.5 million in cash but faces $1.5 billion in CapEx needs through 2026 for satellite deployment.

- Government contracts total $63 million to date, including a $43 million SDA award and $20 million from the DIU.

- Commercial revenue for 2025 is projected at $50–$75 million, largely back-end loaded and contingent on satellite launch cadence.

- Each Block 2 satellite now costs $21–23 million, with plans to deploy over 60 satellites by year-end 2026.

AST SpaceMobile (ASTS) is racing toward something as ambitious as any space-based telecom: developing the first space-based cellular broadband net that directly interfaces with commercial smartphones. Milestones such as recent orders by the U.S. government, two-way space-based video transmissions, and rapid ramp-up of a BlueBird satellite constellation have ASTS ringing the bell for aggressive execution.

Management itself characterizes the current phase as an “inflection point,” with deployment plans of more than 60 satellites throughout 2026 facilitating commercial broadband coverage throughout core geographies. And with support partnerships that range from AT&T, Rakuten, Verizon, and Vodafone, commercial pillars seem solid.

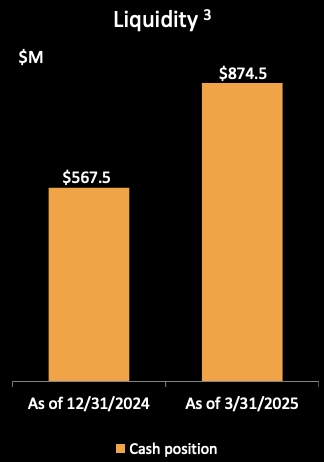

But even as the story is compelling, the valuation data tells a far different tale. Core valuation metrics such as EV/EBITDA, EV/EBIT, and P/E are once again not meaningful (NM), again emphasizing the pre-revenue nature of the business. Even with an impressive $874.5 million liquidity at Q1 2025, increasing CapEx and a lack of near-term profitability create significant questions concerning the financial viability of its vision. This disconnect between narrative traction and financial foundations is an important quandary for investors.

Source: AST SpaceMobile, First Quarter 2025

At its heart lies the trade between ASTS’s asymmetric potential, it may potentially rebuild mobile connectivity if successful, and the enormous valuation risk that depends on flawless execution amidst merciless capital markets. Having only 2025 forward revenue of $50–$75 million, ASTS is pricing victory years before delivery. Investors are asked to pit first-mover momentum and governmental traction against exploding costs, a slender revenue model, and a valuation that’s off the scale.

A Roadmap to Space: AST SpaceMobile’s Ambitious Business Model

AST SpaceMobile’s ambitious vision is to abolish mobile dead zones throughout the world with a constellation of satellites that communicate directly with commercial off-the-shelf smartphones. While legacy satellite architectures require proprietary devices or ground terminals, ASTS is developing a direct-to-device (D2D) architecture that operates over licensed wireless spectrum bands with assistance from Tier-1 mobile network operators (MNOs). In that respect, ASTS stands out from incumbent players like Iridium, Globalstar, and Starlink, with ASTS functioning as a telecom disruptor rather than a pure satellite player.

These Block 2 BlueBirds, with their huge phased-array antennas, are at the heart of such a capability. With up to 2,400 square feet of surface area, 100 times that of the prior BlueWalker 3 satellite, these satellites are capable of providing broadband-level speeds and persistent coverage. Defined by management is an implementation plan consisting of deploying five such satellites within the next six to nine months, ramping up to 60+ by year-end 2026. A six-satellite monthly cadence is targeted by an internally aligned, vertically integrated approach to manufacturing with internally executed phased array assembly and solar panel integration.

Aside from commercial goals, ASTS is collaborating with U.S. government agencies for the provision of defense-grade communications by sea, air, and land. The company secured the contract for $43 million with the U.S. Space Development Agency and recently secured another new contract for $20 million via the Defense Innovation Unit (DIU). These are valuable tech endorsements that could potentially provide the foundation for future recurring revenues.

Yet despite the progress, the business model remains in early-stage flux. Gateway hardware bookings reached $13.6 million in Q1 2025, with expectations of ~$10 million per quarter throughout the year. However, these hardware revenues are largely one-time and don’t reflect recurring service monetization. The real inflection will come only when cellular broadband subscriptions and usage-based fees kick in, a milestone dependent on both satellite deployment and regulatory approval across markets.

Source: AST SpaceMobile Investor Presentation

Trapped Between Stars and Steel: Valuation Risk Faces Operational Execution

Adding insult to injury is the high capital intensity. First-quarter 2025 CapEx was $124 million, with the Q2 guide raising that amount to $230–$270 million. ASTS even increased its average satellite cost to $21–23 million due to increased launch costs and new tariffs.

.jpg)

Source: AST SpaceMobile, First Quarter 2025

The company’s cash standing at $874.5 million looks good, but cumulative CapEx requirements potentially hitting above $1.5 billion by 2026 could put liquidity at risk should revenue recognition be delayed. While the management has commenced a new ATM facility for $500 million, additional dilution looks inevitable without the arrival of non-dilutive financing from sources such as EXIM or IFC in time.

Operationally, ASTS has yet to demonstrate scalability. While the engineering milestones, the ASIC chip supporting 120 Mbps per cell, and the successful video calls over Block 1 are impressive, the company is only at the beta activation level. The commercial revenue estimate of $50–$75 million for 2025 is “back-end loaded,” subject to successful Block 2 satellite deployment, completion of U.S. government milestones, and gateway partner monetization. That would mean potential delays in launch cadence or regulatory approvals would negate full-year revenue assumptions.

Riding the Government Tailwind, but Facing Commercial Gravity

AST SpaceMobile’s value proposition finds support in increasing governmental interest in sturdy, space-based communications infrastructures. It's a new up-to-$20-million DIU contract that follows the previously announced $43-million contract with the Space Development Agency, suggesting national security deployments could provide ASTS with valuable revenue apart from the traditional commercial telco partnerships. These contracts are both funding mechanisms and strategic endorsements, especially because the U.S. is considering space-based redundancy for terrestrial infrastructures.

However, this tailwind is dampened by considerable risks along the commercial path. While MNOs like AT&T and Vodafone have shown successful video calling with ASTS satellites, the transition from test to revenue-bearing service is by no means guaranteed. Sales from such Tier-1 operators are conditioned upon performance SLAs, regulatory approvals, and harmonizing spectra between jurisdictions. Moreover, ASTS must negotiate complicated partnerships between highly dissimilar markets, like the United States, Japan, and Europe, with their respective spectrum policy regimes and technical requirements.

Regulatory progress is promising, but is only partial. Special Temporary Authority (STA) at the FCC was granted to the company for testing across Band 14 (public safety spectrum), agreements for up to 45 MHz mid-band spectrum have been undertaken, and coordination agreements with the National Science Foundation have been formed. Although commercial-scale nationwide service depends on securing additional clearances across important markets, aiming at commercial launches and regulatory milestones at the same time makes such a plan even more capital-intensive with operational risk.

Inflection point argumentation, though seductive, blurs execution risk. Management is unfazed, but investor Q&A during the Q1 2025 earnings conference call voiced concerns over rising launch costs, geopolitical increases in tariffs, and capital dilution. Analysts challenged navigating rising costs, and CFO Andrew Johnson agreed that “this is a dynamic situation” with respect to launch vehicle costs and tariffed inputs.

Conclusion: A Tethered rather than Rocket-Scaled Opportunity

AST SpaceMobile resides at the crossroads between aspiration and valuation gravity. The firm is executing across various fronts, from satellite construction to U.S. government business, but resides in the early innings of commercial validation. Long-term platform potential resides within the business model, especially in underserved markets and defense business cases. However, the valuation assumes ideal execution and monetization of a yet-beta product, leaving it at high risk even for asymmetric players. Unless ASTS is successful in converting its launch cadence, the government orders, and MNO alliances into recurring, scalable revenues by the end of 2025 or during 2026, the present valuation shall not be perpetuated. Speculative players may be looking at the formation of a multi-bagger, but institutions shall demand progress on monetization and margin stabilization before reassessing valuation upside. With current prices, the stock embodies more hope than reality.

Copyleaks Report: https://app.copyleaks.com/report/10kv4osttsschjj0/preview?key=vy29xvgxg36z1n2j&viewMode=one-to-many&contentMode=text&sourcePage=1&suspectPage=1&showAIPhrases=false&alertCode=suspected-ai-text

.png)

Get Started

Find out more