"Stablecoins as Platforms": Why Every Company Needs a Stablecoin Strategy

Original Title: "Stablecoins are a New Platform"

Author of the Original Article: Simon Taylor

Translated by: Block Unicorn

Preface

Every fintech company is going to become a stablecoin company. While stablecoins have sparked a mix of hype, skepticism, hope, and concern, I believe we've reached a significant inflection point. We’ve transitioned from the era of "Banking-as-a-Service" (BaaS) to an era where stablecoins serve as foundational infrastructure. Consumer (B2C), enterprise (B2B), and infrastructure companies built around stablecoins will shape the industry in the next decade.

This shift will be 10 times more transformative than the fintech boom of the past decade, as we are heading toward a new layer of infrastructure. Many currently view stablecoins merely as a new payment channel, but once they’re recognized as a platform that sits atop every other layer, the industry will fully transition to a stablecoin-native ecosystem. Stablecoins are a platform.

Key Takeaways:

· The previous era: Banking-as-a-Service (BaaS) and its implications for stablecoins

· Why stablecoins are an infrastructure layer (and not just another channel)

· The stablecoin gold rush and implications of regulatory unlocks

· Full-stack use cases

· Strategic positioning and future outlook

1. Lessons Learned from BaaS to Stablecoins

As the saying goes, fools rush in. We've seen this play out in BaaS. The 2010s era in financial services was characterized by companies adopting mobile-first distribution models and cloud-first infrastructures.

We witnessed the emergence of a generation of new infrastructure providers purpose-built for financial services. APIs made every bank department and IT system accessible—from customer onboarding, anti-fraud, anti-money laundering (AML), and card issuance, to, in some cases, even customer service. This allowed new companies to launch mobile apps, wallets, and "accounts," enabling them to acquire and serve customers at a fraction of the cost compared to legacy institutions.

By combining APIs, mobile, and cloud technologies, fintech companies also benefited from the support of a handful of "sponsor banks" that saw the opportunity to provide banking rails, store funds, and facilitate fund transfers to this burgeoning field. Some banks thrived by becoming known as "easy to work with."

Image Source: Klaros Partners

For fintech companies, their initial business models are:

· Generating revenue through interchange fees

· Reducing customer acquisition cost (CAC) via frictionless digital onboarding

As the saying goes: "Show me the incentives, and I'll show you the outcome." Some (not all) fintech companies have optimized for conversion rates. When you do this, many norms of financial services begin to appear as friction. For example, requiring customers to provide multi-page documents for "Know Your Customer" (KYC) checks or monitoring transactions for international terrorism risks, even though the vast majority of customers are domestic.

When I penned "BaaS is Dead" in March 2023, we had already started seeing ominous signs. Account openings are a crucial touchpoint for both sides when it comes to catching bad actors. If you view account openings as a checkbox process that must be completed with minimal friction, a minimalist interpretation of Bank Secrecy Act/Anti-Money Laundering (BSA/AML) rules can lead to a high-conversion onboarding flow. Over the past two years, this has allowed fraud and money laundering to scale remotely, exploiting the weakest parts of the system. —Excerpt from "BaaS is Dead"

If you're a bad actor, targeting small new banks and digital banks is a no-brainer. But the outcomes are not good. On April 22, 2024, Blockchain-as-a-Service (BaaS) provider Synapse went bankrupt, leaving tens of thousands of customers without access to their life savings. Fintech apps were unable to access these funds, and the underlying banks couldn't trace or reconcile the destinations of the funds.

This incident made headlines in mainstream media. Within the banking sector, regulators issued a series of consent orders that highlighted deficiencies in:

· Third-party risk management (i.e., API providers and fintech companies)

· Anti-money laundering (i.e., inconsistent controls within these companies)

· Board governance (i.e., whether management was held accountable)

Image Source: Klaros Partners

The consequences of these failures are massive. If you can't stop the flow of money to bad actors, criminals get paid, effectively funding human suffering. However, the lesson here is not that BaaS or fintech is inherently bad; quite the opposite.

Today, we have:

· The ability for immigrants and low-income individuals to open free accounts

· The ability to approve loans using cash flow (the money you have), which means more people can avoid bankruptcy

· Great spend management cards

· Embedded lending solutions for marketplaces, SMBs, and vertical SaaS

Successful major financial brands have reshaped the industry. Cash App, Venmo, Chime, Affirm, Revolut, Monzo, Nubank, Stripe, Adyen, and your favorite brands have become household names in their markets and industries. Fintech has fundamentally changed the way finance is distributed and raised the bar for user experience.

We’ve simply picked up a few lessons along the way. The investment scale and cross-border activity of stablecoins could result in any crash having epic consequences. While I know that it’s impossible to completely prevent bad events, I hope companies centered around stablecoins can learn from the mistakes and successes of the BaaS era and not get swept up in the gold rush on the horizon.

2. Regulatory Unlocks and Capital Surge

2.1 Regulatory Unlocks

The current draft proposal of the GENIUS Act could change everything. According to the proposal, if you’re an approved stablecoin issuer, you can classify stablecoins as cash equivalents on your balance sheet. This is a big deal. Take prepaid cards as an example. They require money transmission licenses, refund rules, and consumer protection requirements. Cash, on the other hand, is as simple as the cash in your pocket—it’s significantly easier to hold and manage. Stablecoins could inherit this simplicity.

2.2 The Stablecoin Gold Rush

Funding in stablecoin-related businesses is expected to grow 10x year-over-year.

Funding status of stablecoin-related businesses

If the GENIUS Act passes, a new regulated stablecoin channel and a new narrow banking category called Permitted Payment Stablecoin Issuers (PPSIs) will emerge. This means every entrepreneur, venture capitalist, payments company, shadow bank, and even traditional banks will act to defend or seize this new opportunity.

3. Argument: Stablecoins as a Platform

Today, stablecoins are being used as alternative cross-border payment channels, and in the future, they are likely to become domestic payment channels. But if you only view them this way, you’re missing the bigger picture. Stablecoins are also a platform that operates above channels like SWIFT, ACH, PIX, and UPI, becoming the infrastructure to connect all these channels. This will unlock new use cases and opportunities.

Ultimately, stablecoins will create an abstraction layer on top of existing payment channels, much like what the internet did to telecom operators. Similarly, the entire industry will become "stablecoin-ized," akin to what we observed with video, messaging, and e-commerce. This network layer will eventually eliminate intermediaries and reduce costs. — Excerpt from "Stablecoins Aren’t Cheaper; They’re Better"

Here’s how I envision it:

Stablecoins as a Platform

This is what platform disruption looks like. Telecom traffic grows 60% year over year, while revenue grows just 1% year over year. Over 15 years, traffic growth has outpaced revenue growth by more than 1000x.

Existing businesses that cannot adapt to the new platform layer will become commoditized. The impact of stablecoins on payments will mirror the impact of the internet on telecom—creating a platform layer that renders the underlying infrastructure into mere commodity pipes. We can see this infrastructure layer gradually emerging in every payment process and business model. Here's how it works.

4. How Stablecoins Function Across the System

Yes, today stablecoins operate as an alternative payment channel. But this is just the foundation. Most people view them as the payment channel depicted in the image below, rather than as a platform:

Stablecoins as Payment Channels—They're not just that; they are much more.

The real opportunity lies in the functionalities they unlock as infrastructure.

4.1 Stablecoins for International Payments—The Starting Point

Unquestionably, the primary use case for stablecoins today is cross-border payments. Major currency corridors include Asian countries, followed by the U.S. to Latin American countries (Mexico, Brazil, Argentina).

G20 Leading Payment Activity to the Global South Through Tron and Tether

There are multiple types of cross-border payments. Let’s delve into each payment flow.

Early Use Cases for B2B:

· Market expansion for scaling enterprises (e.g., SpaceX): Used for financial management, supplier payments, and intercompany settlements.

· International payroll and payments (e.g., Deel, Remote): Payments by contractors and employers are routed to stablecoin wallets.

Artemis surveyed over 30 companies involved in stablecoin-related businesses and found that B2B as a category is growing at a year-over-year rate of 400% (and accelerating), making it the fastest-growing category. (Note: The transaction volume shown in the graph below represents only a portion of the overall market.)

As illustrated by the growth curve, this is significant growth. Currently, last-mile liquidity and foreign exchange spreads remain bottlenecks, but new entrants like Stablesea, OpenFX, and Velocity are entering the market to address these challenges.

Cross-border stablecoin use cases for consumers include:

· Remittances and P2P (e.g., Sling Money): Customers use stablecoins to transfer funds cross-border faster and often at a lower cost.

· Stablecoin-linked cards: Also known as “dollar cards,” they allow consumers in global south countries to pay for services like Netflix, ChatGPT, or Amazon.

Artemis' study further reveals that P2P and stablecoin-linked cards exhibit year-over-year growth exceeding 100%, processing at least $1 billion in transaction volume (TPV) within the sample group. Stablecoins are increasingly becoming a feature for neobanks (e.g., Revolut and Nubank). While current use cases are still relatively narrow, their potential for expansion in the future is significant. Apps like Revolut, which originally built their platform around remittances and P2P, stand to capitalize on this emerging channel due to their unique positioning.

Currently, foreign exchange spreads for local currency transactions are often high, with limited liquidity. However, this scenario is evolving. The domestic payments landscape is still taking shape, but it holds significant intrigue.

4.2 Stablecoins for Domestic Payments (Future Directions)

Domestic B2B use cases include:

· 24/7 yield-bearing stablecoins (e.g., ONDO or BUIDL): At present, crypto-native financial teams convert stablecoins into tokenized treasuries to avoid exchanging them for fiat. If such 24/7 functionality can be integrated into enterprise resource planning (ERP) systems, it could be incredibly appealing to any corporate financial officer.

· Stablecoins as an alternative to FBO structures (e.g., Modern Treasury): One characteristic of U.S. regulation is that non-bank institutions facilitating fund transfers on behalf of customers typically require a "For the Benefit Of" (FBO) account structure. These account setups can be complex. Modern Treasury's stablecoin product allows financial teams to set up payment workflows for customers without the need for FBO structures.

· Stablecoin-native B2B accounts (e.g., Altitude): "Borderless accounts" provided by companies like Wise or Airwallex could be natively powered by stablecoins. These accounts would primarily operate in USD but come with front-end tools to manage invoices, expenses, and financial operations.

Domestic consumer use cases are still in their early stages and include:

· Stablecoin-native "checking" accounts (e.g., Fuse): These would offer a consumer experience similar to Wise, Revolut, or remittance apps, but with a default global orientation. Services like these currently appear in countries in the Global South, but they could represent a new, low-cost model for consumer fintech projects.

· Prepaid card programs: Since stablecoins can function as cash equivalents, finance managers can bypass the complexities of managing prepaid liabilities while gaining programmable currency that functions like cash in the balance sheet but flows like digital payments.

· P2P stablecoins: Applications like Zelle, Venmo, Pix, and Faster Payments dominate in their respective domestic markets, but if stablecoins evolve as an alternative, these applications might simply serve as front-end interfaces supporting them.

4.3 Financial and Infrastructure (Hidden Layer)

The hidden layer refers to infrastructure. Banking technology itself is becoming native to stablecoins.

· Stablecoin issuance-as-a-service (e.g., Brale, M^0): Banks and non-bank institutions may want to issue their own stablecoins to attract deposits or to avoid fees charged by other issuers.

· Stablecoins as a side core (e.g., Stablecore): Banks might want to create a record-keeping system that interacts with stablecoins but remains independent of their traditional platforms. A "side core" accomplishes this while still reconciling with the main core system.

· Stablecoins provide infrastructure similar to BaaS (e.g., Squads Grid): Offering developers simple APIs to quickly create consumer, B2B, or embedded financial products.

Most companies in the market are vastly underestimating how much developers appreciate the convenience of stablecoins. For companies like Stripe, convenience has always been the key to success. You can imagine other possibilities. As a thought experiment, think of stablecoins as a global, programmable ledger system where everyone can reconcile and view transactions. Each wallet address can be assigned to a known frontend or wallet creator, enabling these entities to collaborate instantly when KYC or AML issues arise.

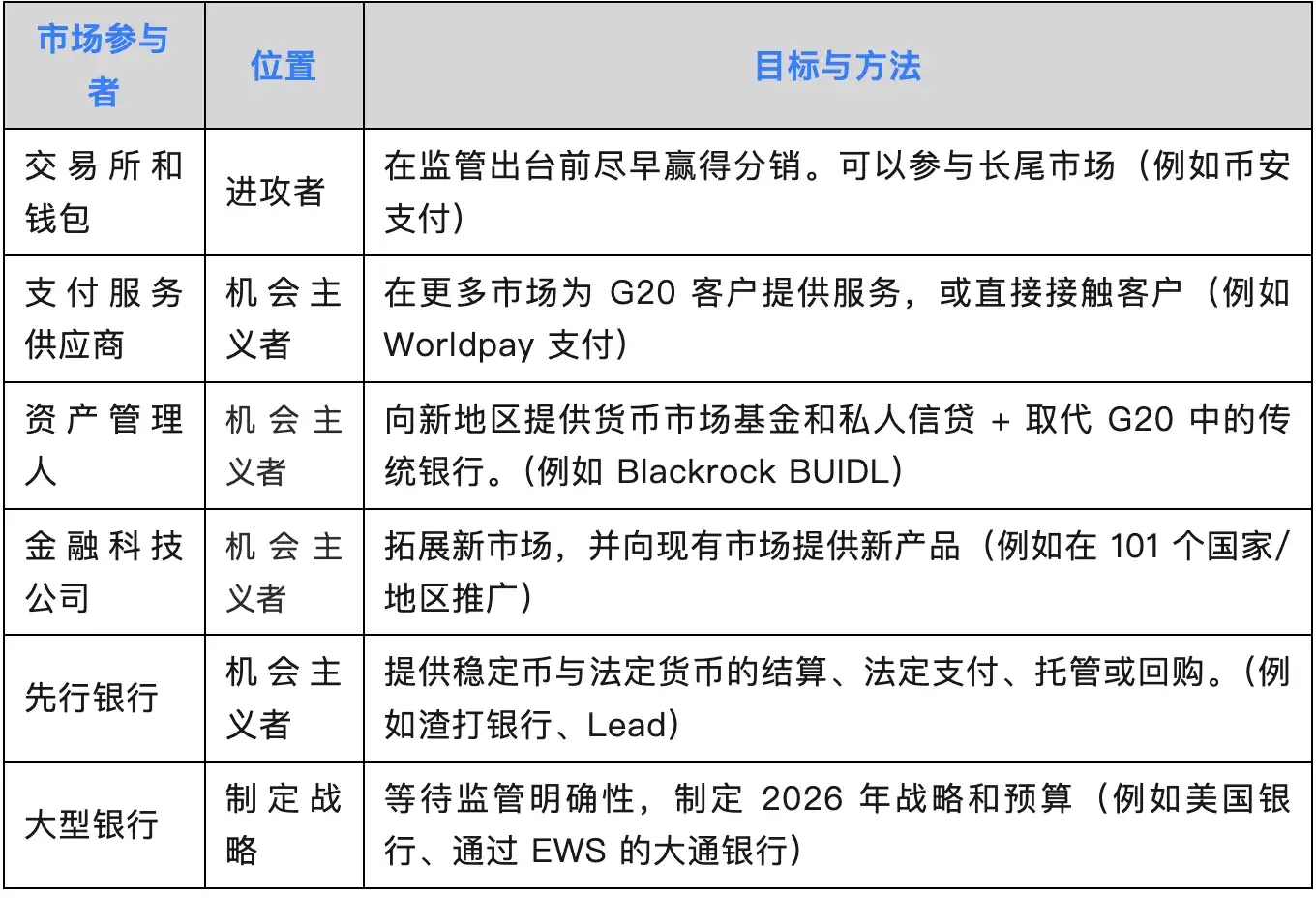

4.4 Strategic Positioning of Stablecoins

The current market consists of aggressors, opportunists, and participants who are still observing and formulating strategies. At present, the overwhelming majority of activity is happening on new platforms like crypto exchanges and wallets. However, the opportunists are companies now positioning themselves to leverage stablecoins as new payment rails:

Here are my thoughts on who falls into which category:

Aggressors:

· Asset management firms such as BlackRock, Franklin Templeton, and Fidelity, which rely on banks for wire transfer settlements. Since the financial crisis, they have been taking market share in credit and money market funds from banks. Stablecoins tie all of this together through an instant, 24/7 settlement layer.

· Payment companies such as Stripe, WorldPay, and Dlocal are expanding the number of markets they can operate in and the types of payment workflows they provide. "Financial accounts" erode the core business of large money-center banks but typically target newer customer segments.

Defenders:

· Large banks: Institutions such as JPMorgan Chase, Bank of America, Citi, and other U.S. banks have previously discussed launching their own stablecoins. I think this may be an attempt to capture a share of the market for this new domestic and cross-border payment "channel." Just as banks have dominated P2P payments through Zelle, they may "inevitably" dominate this new channel as well.

· Smaller banks: These institutions have started lobbying against stablecoins. Stablecoin issuers, asset management firms, and large banks could siphon deposits away from their lower-yielding checking accounts, making smaller banks the biggest losers in this scenario.

There will be a wave of opportunistic banks, similar to what we've observed with correspondent banking, that will seize significant opportunities through the disruption brought by stablecoins. The reality is that opportunities vary depending on the use case. Startups are exploring new payment workflows, while Payment Service Providers (PSPs) are expanding market access through existing processes. In the future, asset management companies and banks will find their place in the market, likely closer to their existing core businesses.

5. Criticisms, Concerns, and Why Most Are Overblown

I have summarized the criticisms as follows:

· Criticism: Stablecoins will trigger a bank run scenario. Counterpoint: This assumes Terra-style algorithmic stablecoins, rather than Treasury-backed, permissioned Payment Stablecoin Issuers (PPSIs) under the GENIUS Act.

· Criticism: Big tech companies will form monetary oligopolies. Counterpoint: This is a valid concern, but the framework makes it unlikely for big tech companies to directly issue stablecoins—they are more likely to use stablecoins rather than issue them. Becoming a PPSI involves high regulatory barriers for them.

· Criticism: It will cause community banks to lose deposits. Counterpoint: Money market funds are already contributing to this. Community banks that adapt to offer stablecoin services will thrive.

· Criticism: "This is cryptocurrency," meaning it's riddled with crime and scams. Counterpoint: It’s time to move past this perception. The future of finance is on-chain, and institutional capital is building the infrastructure. There are genuine and novel risks, such as key management, custody, liquidity, integrations, and credit risks, which deserve focus.

· Criticism: Stablecoins are just regulatory arbitrage because "holding USDC shouldn’t be easier than holding dollars." Counterpoint: Fintech itself was built on regulatory arbitrage through the Durbin Amendment. Development is easier on stablecoins, but they are subject to a full licensing regime.

I believe this debate will continue. Stablecoins are poised to drive the next era of finance, and our vision of the future is just beginning.

6. Finally, Why Every Company Needs a Stablecoin Strategy

Everything we are doing today is aimed at realizing the native adoption of stablecoins, which will endow finance with superpowers. We can build instant, global, 24/7 financial systems. We can reassemble financial LEGO bricks while making it more developer-friendly. The BaaS era has shown us that new infrastructure creates tremendous opportunities and significant risks. Companies that learn from the successes and failures of this era will emerge victorious in the stablecoin-centered era.

Every company needs a stablecoin strategy. Every fintech company, every bank, every finance team requires one. This is not just a new payment channel. It is the platform layer upon which everything else will be built. I urge every reader to construct based on the lessons of the past. Crashes are inevitable. Things will go wrong—that's a certainty. This also includes planning how you will protect yourself when things inevitably collapse.

Build cool things. And stay safe.

Original Article Link

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10