TradingKey - As of March 31, 2025, Warren Buffett’s Berkshire Hathaway holds a $258.7 billion equity portfolio spread across 36 stocks. The Oracle of Omaha hasn’t made a new buy this quarter, and turnover remains minimal at 1%. But beneath that still surface lies a quietly evolving strategy shaped by rising rates, sector rotations, and valuation discipline.

An Under Pressure Legacy Portfolio

Buffett's biggest position is still Apple (AAPL), holding 25.76% of the portfolio or $66.6 billion. Cracks are appearing, though. Apple fell 12.45% YTD, lagging the wider market following iPhone selling declines and regulatory threats. Berkshire has not reduced its holding, but the size of this holding is becoming a double-edged sword, still cash-generating, but less of a growth vehicle than it was in previous years.

Buffett's relative underperformance serves to reinforce the overall theme of 2025: resilience rather than reinvention. Other funds are moving toward AI companies and turnarounds, but Berkshire is embracing stability instead. Trade-offs, however, accompany this approach. Concentration within the portfolio has picked up, and the diminishing weight of Apple has pulled down aggregate performance.

.png)

American Express, Coca-Cola, and the Moat Mentality

Two of Buffett's most famous holdings, American Express (AXP) and Coca-Cola (KO), are worth 15.77% and 11.07% of the portfolio, respectively. Both are showing once more why Buffett values moats and brand strength. American Express has had modest appreciation in price and sticky consumer outlays, keeping Buffett safe during the tech downtrend. Coca-Cola, meanwhile, is 6.87% higher YTD, thanks to global reopening patterns and inflationary environment pricing power.

Legacy bets are ballast in uncertain times. But they are also reflective of a larger Berkshire maxim: bet on what you know, stay in patiently, and earn dividends along the way. It’s not one which gets the AI-starved investor’s pulse racing, but it’s one which works notwithstanding.

.png)

Energy Bets: A Contrarian View Under Siege

One of Buffett's energy stocks, Chevron (CVX), and Occidental Petroleum (OXY) have fallen in 2025 by 12.25% and 14.15%, respectively. Together, they constitute almost $33 billion of the portfolio, with Occidental accounting for as much as 26.9% of company ownership alone. Whereas oil prices have stabilized, the larger ESG theme plus diminishing upstream margins are being felt.

Berkshire's argument, that fossil fuels are still needed, particularly in underinvested production basins, is unscathed. But the market is not yet rewarding patience. Berkshire added modestly to its stake in Q1 (+763K shares), which demonstrated ongoing faith, but this wager is being tested more than others.

.png)

Financials: Subdued Cuts and Defensive Posture

Berkshire cut its holding in Bank of America (BAC) by 7.15% during Q1 2025, lowering exposure to the holding which is now worth $26.4 billion, or 10.19% of the portfolio. The bank's slight YTD loss (-0.45%) is in line with sector-wide pressures ranging from rising funding to sluggish loan expansion.

Moody’s (MCO) is, though, left unscathed and unchanged at 4.44% of the portfolio. The rating agency business offers recurring cash flows, which are attractive to Buffett’s preference for capital-light enterprises. Mid-tier holdings are rounded out by Chubb Ltd (CB) at 3.16% and DaVita (DVA) at 2.08%. Of note is that DaVita was reduced several times during Q1 and May 2025, likely due to compressed margins and reimbursement risk. The gradual trimming reflects Buffett aggressively eliminating underperformers, although he’s not aggressively making new bets.

Turnover Relates to Your Business Story

Though Q1 had no new buys, Berkshire's turnover history needs to be read between the lines. The collective amount of the fund has declined to $258.7 billion from the levels of $351.9 billion in late 2023, down by almost $93 billion over five quarters. The reason was not aggressive selling, but rather the interplay of mark-to-market losses combined with disciplined trimming. Turnover is still very-low at 1%, sustaining Buffett’s risk-averse image. With this complacency, though, comes reduced exposure to emerging trends like AI, cloud infrastructure, and semiconductors. With Nvidia becoming the new Apple, Berkshire’s aversion to risk can be seen as increasingly dated to newer generations of investors who crave the latest innovation.

Strategic Additions: A Few, but Notable

There are some repositioning signs to be seen. Notable additions are: Constellation Brands (STZ): A significant leap (+113%) to 12M shares evidencing added investment in premium beverage plays. Both Domino's Pizza (DPZ) and Pool Corp (POOL) moved higher, signs of selective consumer-facing exposure in scalable, asset-light business models. Sirius XM (SIRI) and Heico Corp (HEI.A) added pretty modestly, small plays, perhaps, but could be testing grounds for broader conviction. These do not amount to much in dollar terms but are worth noting. Buffett can selectively be experimenting with newer ideas without rocking the core.

Risk Factors: Concentration, Succession, and Business Cycles

Concentration risk becomes apparent here. Near enough to 53% of Berkshire's investment holdings reside in only three holdings: Apple, American Express, and Coca-Cola. That gives it stability, but also vulnerability should one of them decline (like Apple now). There is still succession uncertainty. Even though Greg Abel is widely being considered to succeed, institutional investors are not certain as to whether the investment style's continuity after Buffet is secured. Will the next generation be as conservative as Buffett, or transition more aggressively? Long at last, market cycle sensitivity has returned.

Berkshire's excess exposure to consumer, energy, and finance makes it more defensive but less responsive to secular trends dominant in the market presently, such as green energy, cloud computing, and artificial intelligence

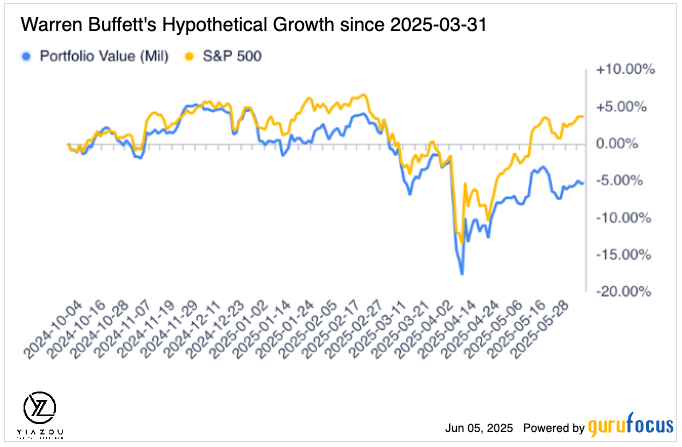

Performance versus the S&P 500: A Mixed Bag

Berkshire has posted decent returns in recent times, 25.5% in 2024 versus 23.3% for the S&P 500. Its long-term performance, however, has been less stellar in recent tech-fueled bull cycles. It returned 15.8% in 2023, behind the 24.2% gain of the S&P. It lagged by over 13 and 17 percentage points in 2020 and 2019, respectively.

However, its ability to thrive in down years (i.e., 2022: +4% vs. S&P -19.4%) is one of its long-term attractions. Berkshire won't always be first in bull periods, but it generally doesn't lose the bear wars.

Final Reflections

Warren Buffett's portfolio in 2025 demonstrates staying power, discipline, and conviction, mixed with restraint in a fast-moving market. His core holdings continue to generate consistent cash flows, though without the buzz around newer, AI-touted stocks. Buffett's critics may see the portfolio trailing innovation in this age. His supporters, however, will argue it's a masterwork of stability, precisely appropriate for unstable times. Either, it's a functioning case study in long-term investing, a reflection of the man who made it. The message is one which is clear to long-term investors and allocators: compounding is strongest when it is accompanied with patience, and, at times, avoiding the hot hand can be the most aggressive step of them all.

Find out more