Key Takeaways

- Business Model: UnitedHealth's vertical integration model drives efficiency but faces ethical, regulatory, and reputational challenges.

- Optum's Growth: Optum's rapid growth, especially in pharmacy and healthcare services, is offset by setbacks in data analytics and rising compliance costs.

- Valuation: Despite a 60% stock price drop, valuation estimates $322-$350 suggest risks are priced in, with growth recovery expected by 2026.

Once a Wall Street sweetheart, UnitedHealth Group (UNH) dominated the US healthcare industry with its unbeatable vertical empire, spanning insurance, clinics, pharmacies, and data analytics. Its stock skyrocketed 600% in a decade, making it a must-own blue chip. However, in 2024, the empire cracked. Regulatory crackdowns, sinking profits, and executive chaos sent shares plunging. Now, investors are split: Is this a historic buying opportunity… or the beginning of the end?

Source: TradingKey

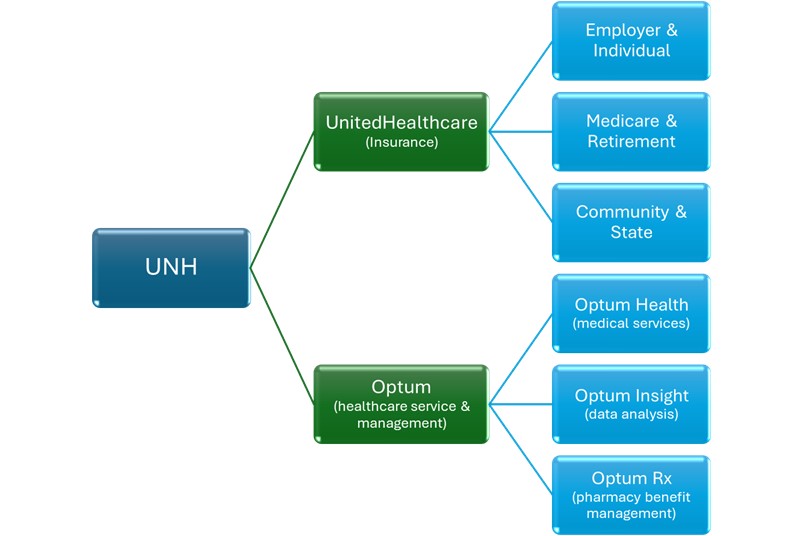

UNH's Business Model: Playing Both Judge and Player

UNH operates a highly controversial yet highly profitable business model: It acts as both the insurer (UnitedHealthcare) and the healthcare provider (Optum). This vertical integration was once hailed as the future of healthcare, but now faces intense scrutiny.

Source: TradingKey

Cost Savings: Optum directly manages doctors, clinics, and pharmacies, optimizing resources and reducing waste. It promotes value-based care, where payments are tied to patient outcomes rather than service volume—cutting unnecessary hospitalizations and ER visits. This allows UNH to control costs at both the provider and insurer levels, boosting efficiency.

Data-Driven Decisions: Optum Insights uses big data and AI to streamline claims processing, predict medical needs, and identify high-risk patients early, preventing costlier treatments later.

Diversified Revenue: While insurance remains UNH’s cash cow, Optum’s healthcare services and pharmacy segments are growing fast, reducing reliance on insurance. In 2024, Optum’s profits surged, further balancing the business.

Scale Advantage: With about 90,000 doctors and a vast pharmacy network, UNH dominates the market. Anyone who wants to enter this market faces higher barriers.

However, as you can see, from a commonsense perspective, this model also has big flaws:

Ethical Risks: As both the payer (insurer) and provider (doctor), UNH faces clear conflicts of interest. Insurers profit by limiting payouts, so does Optum prioritize care or profits? A lawsuit in the US District Court for the State of Minnesota accused NaviHealth, a subsidiary of UNH, of using algorithms to deny rehabilitation treatment to the elderly, and a report by the US Senate Permanent Subcommittee on Investigations pointed out that NaviHealth's refusal rate for post-acute care services was 3 times the industry average.

UNH's Revenue Breakdown

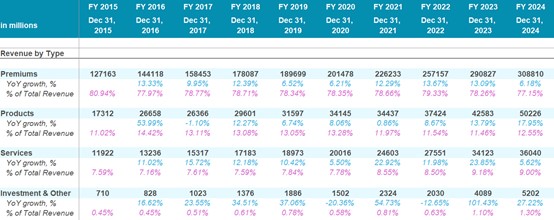

Insurance companies' income mainly depends on customers' premiums and investment income, but at the same time, UNH's medical service platform Optum brings in product and service income, so UNH's income sources are richer than other insurance companies. UNH's money mainly comes from the following: Premiums, Products, Services, and Investment and Other. In 2024, UnitedHealth will achieve a total revenue of approximately $400.3 billion, with revenue mainly coming from the following four parts:

Source: Company Financials, TradingKey

Premiums: Approximately $308.8 billion, accounting for 77% of revenue, serve as UNH's cash cow, generated by its insurance division UnitedHealthcare. In 2023, premiums grew by 13%, primarily driven by increased enrollment in Medicare Advantage (MA), the government-sponsored health plan for seniors aged 65+. However, the decline in the number of MA participants in 2024 contributed the premium growth rate to drop sharply to 6%.

This premium slowdown also stems from Medicare's 2024 transition to the latest diagnosis and procedure coding system, which recalibrated risk adjustment factors and payment weights for certain treatments. Many previously overestimated risk categories were downgraded, meaning patients' risk scores broadly declined. Consequently, insurers like UNH lost reimbursements for conditions that previously qualified for government payments. As the dominant MA insurer, UNH was hit hardest, forced to cover patient costs amid reduced payments. Premiums were reduced and profit margins were squeezed.

Another factor to consider is America's accelerating aging crisis. According to data from the US Census Bureau, the 65+ population surpassed 58 million in 2024 (17.4% of Americans), with seniors typically managing multiple chronic conditions requiring ongoing care. As more high-risk, medically complex patients enroll in MA plans, demand for services has surged. UNH data reveals MA members are using significantly more outpatient visits, hospitalizations, and specialist care, especially as deferred pandemic-era treatments create a backlog, driving UNH's medical costs upward.

Source: Company Financials, TradingKey

Products: Approximately $50 billion, 13% of revenue, which grew 12% in 2024, primarily driven by Optum Rx's pharmacy benefit management (PBM) business. The segment added 750 new clients last year while maintaining an exceptional 98% retention rate. Revenue growth stems from both expanded customer coverage and rising per-member drug utilization, fueled by an aging population's increasing prescription needs. Optum Rx also enhanced operational efficiency through optimized supply chain management and improved delivery networks, enabling higher prescription fulfillment volumes.

A major process innovation was streamlining prior authorization requirements—Optum Rx eliminated pre-approval mandates for ~80 medications. This reduced administrative burdens for doctors/patients while cutting overhead costs, demonstrating how vertical integration creates value.

Services: $36 billion, 9% of revenue generated by Optum's healthcare delivery (clinics/surgery centers) and data analytics (Optum Insight), grew 9% in 2024.

Investments & Other: $5.2 billion, 1% of revenue, primarily investment income, saw slowed growth because when interest rates rise, the market value of the bonds held by UNH declined, resulting in an unrealized loss.

Overall, Optum has not only improved operational efficiency and cost control capabilities through vertical integration of healthcare providers and drug supply chains, but also enhanced its ability to manage patient health, driving rapid growth in service and product revenues, and becoming the core engine of UNH's revenue growth.

UnitedHealthcare vs. Optum: Who makes more money?

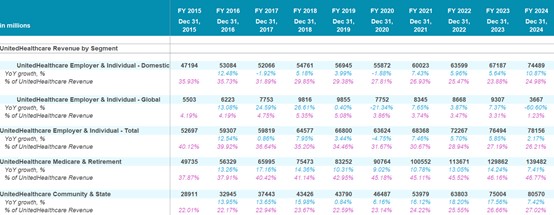

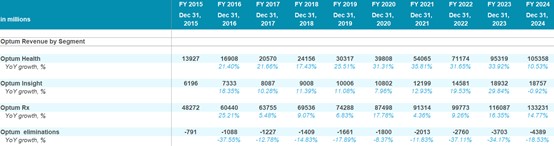

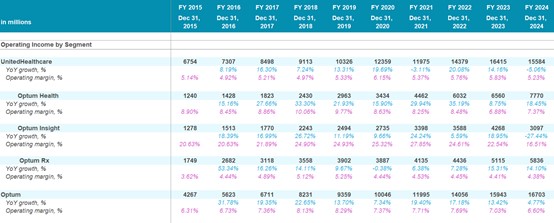

The two pillars of UNH are UnitedHealthcare (insurance) and Optum (medical services). In 2024, UnitedHealthcare's revenue was $298.2 billion, a year-on-year increase of 6%, but Optum's $253 billion in revenue contributed 50% of profits and grew faster.

Source: Company Financials, TradingKey

UnitedHealthcare:

Source: Company Financials, TradingKey

From Employer & Individual Segment, revenue in 2024 is $78.2 billion, up 2%. Among which, global revenue fell by 60% in 2024, not because the company gave up international business, but because the US market is more profitable, the company took the initiative to shrink international business and focus more on the US market.

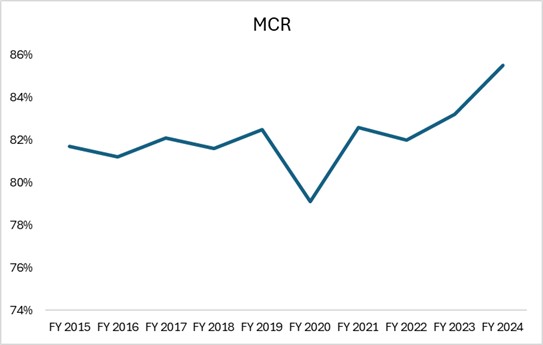

Medicare & Retirement in 2024 is $139.5 billion, up 7%, and is the largest source of income for the insurance sector. It accounted for 46% of insurance income in 2024, driven by aging and Medicare Advantage plans. At the same time, UnitedHealth has an absolute leading position in the Medicare Advantage market. As of March 2025, it has about 9.9 million MA insured persons, accounting for 28.7% of the market, far exceeding the second Humana's 16.6%. Although the overall growth rate of the MA market has slowed down, UNH still maintains growth, reflecting its strong market penetration and customer stickiness. But as mentioned above, costs will soar in 2024, and profit margins will be squeezed. MCR (medical costs/premiums) will rise to 85.5% in 2024.

Source: Company Financials, TradingKey

However, this is not unique to UNH; it's an industry problem that has also hit Humana and CVS, but UNH's size has hurt it more.

Source: TradingView

Optum:

Source: Company Financials, TradingKey

Optum is a healthcare service and health management platform under UnitedHealth Group. Its main businesses cover healthcare service provision, data analysis and technical support, and pharmacy benefit management (PBM). It helps optimize healthcare service efficiency, reduce costs and improve patient health management by vertically integrating medical resources and technical capabilities. Optum is divided into three parts: Optum Health (medical services), Optum Insight (data analysis), and Optum Rx (pharmacy benefit management).

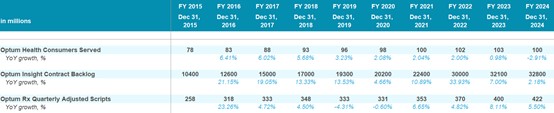

Optum Health: Optum Health is mainly responsible for directly providing medical services, including physician groups, clinics, day surgery centers, specialty clinics and emergency medical centers. In 2024, it served approximately 20 million patients and achieved revenue of $105.4 billion, a year-on-year increase of 11%. Optum Health strives to control medical costs while meeting the growing needs of patients and attracting more customers to join by promoting value-based care models and flexibly adjusting contract payment methods.

Optum Insight: It is the most profitable segment in Optum's business, making money by providing solutions based on big data and AI.

Source: Company Financials, TradingKey

Revenue in 2024 is $18.8 billion, and the revenue growth rate has dropped significantly. At the same time, the profit margin has also dropped from the previous 20% to 17%. The contract backlog (contracts to be executed) has reached $32.8 billion and continues to grow. Although the revenue growth rate has slowed down in 2024, the contract backlog is still high, indicating that the market demand for its technology and services is still strong.

Source: Company Financials, TradingKey

The main reason for the decline in revenue is that in 2024, Optum's Change Healthcare suffered a serious cyber-attack, which caused its medical payment system to be interrupted, affecting its performance, and the Department of Justice investigated the algorithms used by Optum Insight, especially the compliance issues of risk scoring and medical payment. This increased the company's compliance costs and legal risks, forcing the company to invest more resources to meet regulatory requirements.

Optum Rx: Optum Rx is responsible for drug procurement, distribution and management, reduces drug costs through negotiations, optimizes drug use, and simplifies the patient medication process. This segment is the best performing business in Optum in 2024, with operating income of $5.8 billion in 2024, an increase of 14%. In 2024, the prescription volume increased by 15%, and the pre-authorization of 80 drugs (accounting for 10%) was removed. It also reduced consumer drug prices and responded to price increases by pharmaceutical companies. Through large-scale procurement and negotiations, Optum Rx effectively reduced drug costs and returned part of the drug rebates directly to customers to improve price transparency.

Optum is the core driver of UnitedHealth Group's profits, especially the performance of the two high-margin business segments Optum Insight. Although Optum Insight's revenue and profits declined in 2024, it has not risen to the level of illegality, and the company's operations remain normal.

Why did the stock price fall so hard?

After analyzing UNH's business and finances, let's see how serious its problems are. In April, UNH's stock price plummeted 60%, from $600 to around $250. Management even withdrew its 2025 guidance. In summary, UNH is currently facing five major problems:

1. Out-of-control medical costs: In the Medicare Advantage plan, outpatient and specialist medical costs have risen sharply, and new patients have complex conditions and a surge in medical needs, making it difficult for the risk adjustment mechanism to keep up with cost growth. UNH was hit harder by its aggressive expansion, with both insurance claims and medical service costs rising, severely compressing profit margins, but this is a problem for the entire industry.

2. Regulatory storm: The US Department of Justice has launched a criminal investigation into UNH’s Medicare Advantage business for possible health insurance fraud. Although the details of the allegations have not yet been made public, there is widespread concern in the industry that this may be just the tip of the iceberg. As the old saying goes, if you find one cockroach under the bed, there are definitely a million more in the house, and subsequent related allegations and investigations may continue to increase.

3. Fraud rumors: Rumors say UNH is suspected of fraud by double billing for full-risk and self-insured plans; over-billing through its own medical institutions, transferring funds from the insurance side to the medical side, but this is not verified.

4. Public anger: ValuePenguin reported that UnitedHealth's claim denial rate is about 32%, which is twice the industry average. The high insurance claim denial rate makes customers generally dissatisfied with or even hate insurance companies. No industry has ever had customers hate the company that serves them so much.

5. Management trust crisis: CEO Andrew Witty suddenly resigned, citing "personal reasons", but it was obviously related to poor performance. The new CEO Stephen Hemsley is a veteran who tried to stabilize the situation, but market confidence has collapsed.

Can these problems be solved? The rising medical costs and regulatory pressure faced by UNH are common problems for the entire industry, but its vertical integration model makes it bear the dual pressure of insurance claims and medical service costs at the same time, which is riskier. The inherent profit-driven nature of insurance companies leads to their tendency to tighten claims criteria, and this moral hazard exacerbates the conflict between customers and companies. In an environment of increasing aging, rising inflation, possible economic recession, and reduced disposable income, the public has a very low tolerance for insurance denials, anger is easily aroused, and social and political pressure will continue to increase.

If management cannot truly put the interests of patients first and only pursue short-term profits and financial indicators, it will face more severe regulatory and market challenges in the future. AI and new insurance companies may also use AI to optimize claims, reduce denials, improve transparency, and seize market share, thereby accelerating the transformation or replacement of traditional insurance companies.

Are the risks fully priced in?

UNH's valuation needs to be broken down into its insurance (UnitedHealthcare) and medical services (Optum).

- UnitedHealthcare: use P/E valuation. The valuation multiples are conservatively 12 times (the average in the insurance industry is 12-15 times, reflecting the risks of regulation and cost pressure. Management expects operating income to be $16,000-16,500 million dollars in 2025 (take the mid value). In recent years, the effective tax rate is 20-25%. Adding other expenses, the estimated net profit is about 70% of the operating profit. Then the net profit of the insurance business in 2025 is $11,375 million. The 12-times valuation gives a market value of $136,500 million.

- Optum: Using EV/Operating Income for valuation, management expects Optum Health to have an operating profit of $6.2-6.5 billion in 2025, which is a decrease of 18% compared to 2024. Based on this, it is reasonable to speculate that Optum's overall operating profit in 2025 may decrease by 5-15%. That is, the operating profit in 2025 will be $14,198-15,868 million. Conservatively using EV/Operating Income 15 times (the average for the healthcare services industry is 15-20 times), reflecting the current risk, we get an EV of $212,970-238,020 million. UNH's net debt is about $40,000-50,000 million. Similarly, we conservatively remove $50,000 million of net debt and get a market value of $162,970-188,020 million.

Total valuation: Market value of $299,500-324,500 million, corresponding to a share price of $322-350. The lowest price of $250 during the stock sell-off in the past month fully reflects the risk. UNH is expected to resume 13-16% growth in 2026 and will remain a high-quality investment target in the long term.

Find out more