Asian Growth Companies With High Insider Ownership For April 2025

As trade tensions between the U.S. and China escalate, impacting global markets and investor sentiment, Asian economies are navigating a challenging landscape marked by uncertainty and volatility. In this environment, growth companies with high insider ownership may offer a unique advantage, as insider confidence can signal robust business fundamentals even amidst broader market upheavals.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Jolly PharmaceuticalLTD (SZSE:300181) | 23.3% | 26% |

| AcrelLtd (SZSE:300286) | 40% | 32% |

| Arctech Solar Holding (SHSE:688408) | 37.9% | 27% |

| Shanghai Huace Navigation Technology (SZSE:300627) | 24.7% | 24.3% |

| Sineng ElectricLtd (SZSE:300827) | 35.9% | 42.8% |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.3% |

| Laopu Gold (SEHK:6181) | 36.4% | 39.9% |

| Global Tax Free (KOSDAQ:A204620) | 20.8% | 35.1% |

| Synspective (TSE:290A) | 12.8% | 44.5% |

| Fulin Precision (SZSE:300432) | 13.6% | 74.7% |

Click here to see the full list of 637 stocks from our Fast Growing Asian Companies With High Insider Ownership screener.

Let's uncover some gems from our specialized screener.

Xiaomi (SEHK:1810)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Xiaomi Corporation, an investment holding company, offers hardware and software services both in Mainland China and internationally, with a market cap of HK$1.12 trillion.

Operations: The company's revenue segments include Smartphones at CN¥191.76 billion, Internet Services at CN¥34.12 billion, IoT and Lifestyle Products at CN¥104.10 billion, and Smart EV and Other New Initiatives at CN¥32.75 billion.

Insider Ownership: 32.9%

Xiaomi's growth trajectory is highlighted by its forecasted earnings increase of 22.1% annually, surpassing the Hong Kong market average. Recent financial results show a rise in sales to CNY 365.91 billion and net income to CNY 23.66 billion for 2024. Insider buying activity has been positive, albeit not substantial, and no significant insider selling occurred recently. The strategic partnership with NaaS Technology enhances Xiaomi Auto's EV charging solutions amid China's expanding NEV market, positioning Xiaomi well in smart mobility innovation.

- Click here to discover the nuances of Xiaomi with our detailed analytical future growth report.

- Our valuation report unveils the possibility Xiaomi's shares may be trading at a premium.

MIXUE Group (SEHK:2097)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: MIXUE Group is engaged in the production and sale of fruit drinks, tea drinks, ice cream, and coffee products both in Mainland China and internationally, with a market cap of HK$165.13 billion.

Operations: The company's revenue segments consist of CN¥620.05 million from franchise and related services, CN¥23.45 billion from sales of goods, and CN¥756.37 million from sales of equipment.

Insider Ownership: 28.8%

MIXUE Group's recent IPO, raising HKD 3.45 billion, underscores its growth potential in Asia. The company's earnings are forecast to grow at 15.2% annually, outpacing the Hong Kong market average of 10.5%. Revenue is also expected to increase by 13.5% per year, faster than the local market rate of 8.2%. With no significant insider trading activity noted recently and a high forecasted return on equity of 21.8%, MIXUE demonstrates solid growth prospects amidst its evolving capital structure post-IPO completion.

- Navigate through the intricacies of MIXUE Group with our comprehensive analyst estimates report here.

- According our valuation report, there's an indication that MIXUE Group's share price might be on the expensive side.

Kingdee International Software Group (SEHK:268)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kingdee International Software Group Company Limited is an investment holding company involved in the enterprise resource planning business, with a market cap of HK$43.77 billion.

Operations: The company generates revenue from two main segments: Cloud Service Business, which accounts for CN¥5.11 billion, and ERP Business and Others, contributing CN¥1.15 billion.

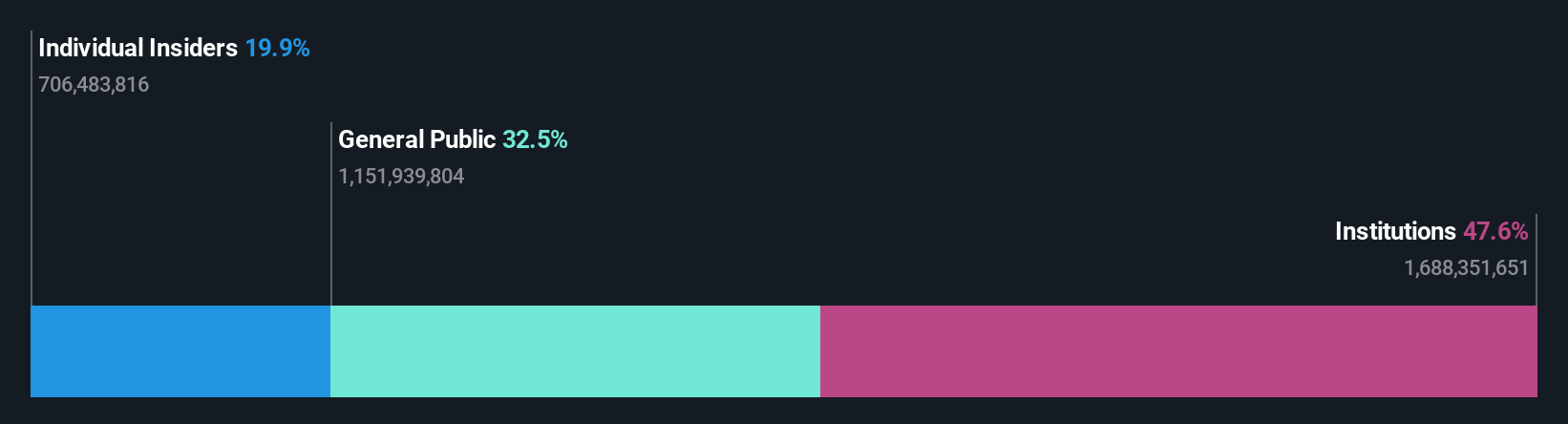

Insider Ownership: 19.9%

Kingdee International Software Group's expansion into the Middle East, supported by a $200 million investment from Qatar Investment Authority, highlights its strategic global growth ambitions. Despite a net loss of CNY 142.07 million in 2024, revenue increased to CNY 6.26 billion. The company is forecasted to achieve profitability within three years and grow earnings at an annual rate of 38.31%, outpacing the Hong Kong market average. Insider trading has been minimal recently, with more purchases than sales but not in substantial volumes.

- Unlock comprehensive insights into our analysis of Kingdee International Software Group stock in this growth report.

- Our expertly prepared valuation report Kingdee International Software Group implies its share price may be lower than expected.

Where To Now?

- Take a closer look at our Fast Growing Asian Companies With High Insider Ownership list of 637 companies by clicking here.

- Looking For Alternative Opportunities? Rare earth metals are the new gold rush. Find out which 21 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Kingdee International Software Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10