Aris Water Solutions, Inc.'s (NYSE:ARIS) Stock Has Shown Weakness Lately But Financial Prospects Look Decent: Is The Market Wrong?

Aris Water Solutions (NYSE:ARIS) has had a rough week with its share price down 20%. However, stock prices are usually driven by a company’s financials over the long term, which in this case look pretty respectable. Particularly, we will be paying attention to Aris Water Solutions' ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

This technology could replace computers: discover the 20 stocks are working to make quantum computing a reality.

How Do You Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Aris Water Solutions is:

8.2% = US$60m ÷ US$735m (Based on the trailing twelve months to December 2024).

The 'return' refers to a company's earnings over the last year. So, this means that for every $1 of its shareholder's investments, the company generates a profit of $0.08.

Check out our latest analysis for Aris Water Solutions

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

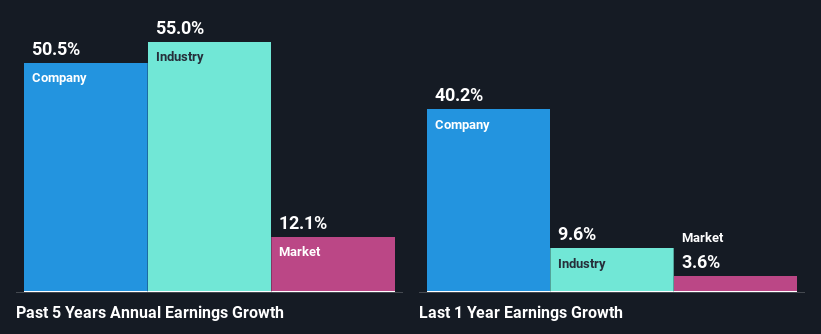

A Side By Side comparison of Aris Water Solutions' Earnings Growth And 8.2% ROE

When you first look at it, Aris Water Solutions' ROE doesn't look that attractive. Next, when compared to the average industry ROE of 12%, the company's ROE leaves us feeling even less enthusiastic. However, we we're pleasantly surprised to see that Aris Water Solutions grew its net income at a significant rate of 50% in the last five years. We reckon that there could be other factors at play here. For instance, the company has a low payout ratio or is being managed efficiently.

We then performed a comparison between Aris Water Solutions' net income growth with the industry, which revealed that the company's growth is similar to the average industry growth of 55% in the same 5-year period.

Earnings growth is an important metric to consider when valuing a stock. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Aris Water Solutions is trading on a high P/E or a low P/E , relative to its industry.

Is Aris Water Solutions Making Efficient Use Of Its Profits?

The high three-year median payout ratio of 61% (implying that it keeps only 39% of profits) for Aris Water Solutions suggests that the company's growth wasn't really hampered despite it returning most of the earnings to its shareholders.

Additionally, Aris Water Solutions has paid dividends over a period of three years which means that the company is pretty serious about sharing its profits with shareholders. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to drop to 40% over the next three years. As a result, the expected drop in Aris Water Solutions' payout ratio explains the anticipated rise in the company's future ROE to 12%, over the same period.

Conclusion

Overall, we feel that Aris Water Solutions certainly does have some positive factors to consider. While no doubt its earnings growth is pretty substantial, we do feel that the reinvestment rate is pretty low, meaning, the earnings growth number could have been significantly higher had the company been retaining more of its profits. Having said that, the company's earnings growth is expected to slow down, as forecasted in the current analyst estimates. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10