3 Reasons to Sell SHYF and 1 Stock to Buy Instead

Shyft has been treading water for the past six months, recording a small return of 0.7% while holding steady at $12.15. The stock also fell short of the S&P 500’s 7.7% gain during that period.

Is there a buying opportunity in Shyft, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

We're cautious about Shyft. Here are three reasons why there are better opportunities than SHYF and a stock we'd rather own.

Why Do We Think Shyft Will Underperform?

Notably receiving an order from FedEx for electric vehicles, Shyft (NASDAQ:SHYF) offers specialty vehicles and truck bodies for various industries.

1. Long-Term Revenue Growth Flatter Than a Pancake

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Unfortunately, Shyft struggled to consistently increase demand as its $787.1 million of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and signals it’s a low quality business.

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Shyft, its EPS declined by 11.8% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

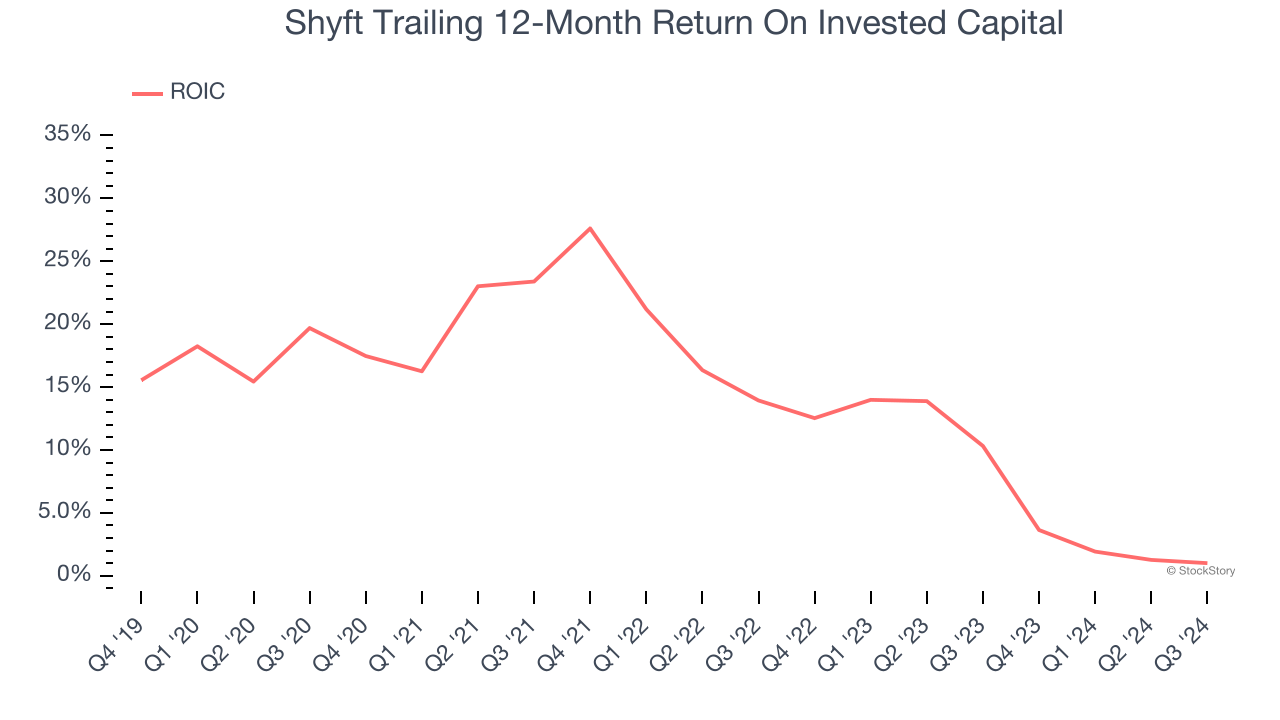

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We typically prefer to invest in companies with high returns because it means they have viable business models, but the trend in a company’s ROIC is often what surprises the market and moves the stock price. Unfortunately, Shyft’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

Shyft falls short of our quality standards. With its shares underperforming the market lately, the stock trades at 17.3× forward price-to-earnings (or $12.15 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are superior stocks to buy right now. We’d recommend looking at Uber, whose profitability just reached an inflection point.

Stocks We Like More Than Shyft

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10